{kind=link}

Image source: Getty Images.

To put it plainly, with limited exceptions, right now is not a great time to buy oil stocks.

How we got here

The past two months have been some of the most volatile and painful in modern oil industry history. The COVID-19 pandemic has resulted in what will surely be remembered as the steepest and fastest decline in global oil demand in history. Here’s a brief overview of the oil market in 2020.

Early February

In its monthly oil markets report, the International Energy Agency (IEA) warned that global oil demand was going to fall due to COVID-19. At the time, the agency said China’s efforts to contain the outbreak of the virus behind COVID-19 would cause a steep drop in that country’s oil consumption, dragging global quarterly oil demand down for the first time in more than a decade.

Late February

After gaining almost 10% in value following the IEA warning under expectations that global producers would cut output, crude oil prices started falling as COVID-19 cases started showing up outside China. Saudi Arabia, along with OPEC, was expected to take 1 million barrels per day in production off the market. If the agreement happened, it would mark at least the third time in five years OPEC had agreed to cut output to stabilize oil prices.

March

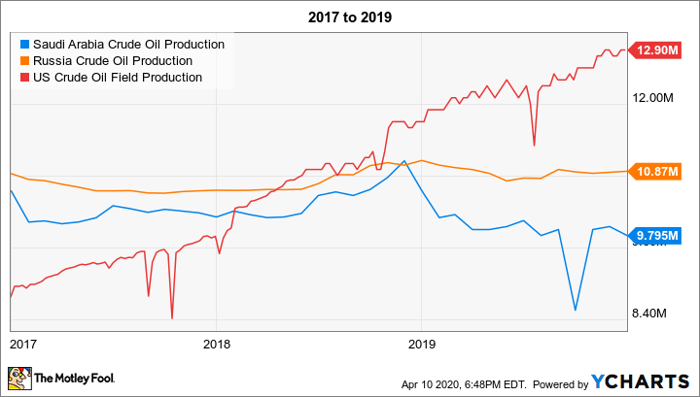

The news got even more hopeful, as OPEC looked to pull Russia into production cuts. Then Russia balked, and Saudi Arabia pivoted from market-stabilizer to all-out war on Russia for global supremacy, catching U.S. shale firmly in the middle. Russia said it would also open up the taps in April once the existing production deal expired, with industry experts pointing to U.S. shale growth in recent years as underpinning Russia’s refusal to cut output.

Saudi Arabia Crude Oil Production data by YCharts

In mid-march, Saudi Arabia raised the stakes yet again. The country’s oil minister said that it would not only increase oil production above 10 million barrels per day in April, but that it would utilize more natural gas for domestic energy, freeing up even more crude oil to sell. In all, Saudi Arabia shifted from commiting to take the bulk of almost 1 million barrels per day in cuts, to saying it would increase its crude exports by more than 40% by May. The United Arab Emirates said it was going to join Saudi Arabia, with plans to increase its oil output by 30%.

By the end of March, oil markets were in absolute turmoil. COVID-19 had become a full-on global pandemic, and global oil demand had already fallen sharply. Airline travel was down 80%. Cruise lines were halting operations. Global shipping was slowing and billions of people were under stay-at-home orders, pulling hundreds of millions of vehicles that consume billions of gallons of fuel off the road.

Things had gone from bad to far, far worse than almost anyone thought they could get. Top oil traders predicted global oil demand would fall 20 million barrels per day, or the equivalent of Russia and Saudi Arabia’s average daily production. Yet Saudi Arabia and Russia continued to make rumblings that they had no plans to cut production, at least without major commitments from others.

April

On April 9, OPEC+ finally reaches agreement to cut 10 production by million barrels per day. On April 10, the G20 met, looking to get commitments from even more global oil players to cut production by as much as an additional 5 billion barrels per day. Combined, the best the world’s biggest oil producers are hoping to reach what would be by far the biggest agreement to reduce output in history.

But it won’t come close to being enough.

The oil market will remain severely oversupplied

There’s no overstating how massive a 15 million barrel per day cut would be, beyond pointing out that terms like “massive” have been used in recent years to describe production cuts of 1.5 million barrels per day, or 1/10 of the size of the hoped-for cuts.

But even these unprecedented production cuts won’t put oil markets back into equilibrium. Global demand predictions of a 20 million barrels per day decline could prove optimistic: More recent projections say demand could crater as much as 35 million barrels per day, with most of global transportation idled and energy consumption under mandatory business closures down sharply. That condition will prove temporary, but won’t end when the calendar turns to May; it’s likely going to take at least until the end of 2020 — and very likely longer — before global energy consumption returns to more normal levels.

In the interim, global oil markets will become increasingly oversupplied, and it’s creating a bigger short-term problem. With the collapse in demand, industry analysts say by mid-may — roughly one month from now — the U.S. will run out of oil storage capacity. Several major U.S. pipeline operators have already started asking their oil producer customers for proof they have buyers for their oil. Over the past two weeks alone U.S. oil inventories increased by 29 million barrels, while gasoline inventories are up 18 million barrels.

The U.S. economy — and hence oil demand — isn’t likely to start recovering in a broad way before June. Los Angeles county just announced an extension to its “stay at home” orders through mid-May, and similar announcements are expected to come from other major U.S. cities and states in the weeks ahead. Put it all together, and even when the economy starts ramping back up, the oil market will still have potentially hundreds of millions of barrels of excess oil inventory to work through. Different scenarios could keep oil demand and prices depressed for the rest of 2020 and potentially well into 2021.

What that means for oil stocks

The companies closest to the oil wells are in the most trouble. West Texas Intermediate crude futures fell below $22 again on April 9, and haven’t been above $40 per barrel since March 6. Many U.S. shale producers need oil to be consistently above $40 per barrel just to cover production costs; when you start adding in debt servicing and corporate expenses, producers are bleeding to death in an environment when there’s nobody to give them an infusion.

We have already seen the first U.S. shale producer fall, with Whiting Petroleum (NYSE: WLL) filing for Chapter 11 bankruptcy protection at the beginning of the month. Whiting reached an agreement with major holders of its debt before filing, that will result in common shareholders losing more than 95% of their stake in the company.

Chesapeake Energy is looking more and more like the next casualty. The company reportedly hired restructuring experts in March, and mutual fund manager Franklin Resources (NYSE: BEN) which owns a substantial amount of both common shares and debt issued by Chesapeake, has reportedly hired a law firm to assist in negotiations with Chesapeake in what could prove to be a pre-negotiated bankruptcy restructuring.

There will almost certainly be more independent oil producers who run out of capital or fall out of debt covenants during this downturn, as there are dozens with similar balance sheet and operating profiles as Whiting. Moreover, many of those also lack the liquidity on their balance sheets to cover even a single quarter’s operating expenses, much less ride out a multi-quarter period of collapsed demand and below-costs oil prices.

And don’t expect to see any bankers riding to the rescue with a lifeline. To the contrary, many banks with large exposure to U.S. oil companies are taking steps to prepare for potentially taking control of assets. According to a Reuters report, JPMorgan Chase (NYSE: JPM), Wells Fargo (NYSE: WFC), Bank of America (NYSE: BAC), and Citigroup (NYSE: C) are planning to create stand-alone businesses to run any oil assets they may seize, looking to get through the downturn instead of offloading oil assets at pennies on the dollar in the current environment.

And it’s not just the oil producers at risk. Their struggles trickle down to the companies they hire to drill the wells and provide the things needed to produce oil like well pipe, drill bits, frac sand, and a hundred other things. Producers are already calling suppliers to put on the squeeze for lower costs and ending contracts early.

Looking further from the oilfields, even refiners, an industry that’s generally quite stable and cash-flow positive, could be at risk under the crushing decline in demand. Refiners count on steady demand that keeps their operations pretty constant to make money.

Even the midstream companies that own the pipelines, gathering systems and storage facilities aren’t perfectly insulated. Long-term contracts won’t serve much good if the producer is insolvent and doesn’t have a buyer for the oil they send down your pipeline. We have already seen several midstream companies cut dividends, and it’s likely that a lot more will follow.

Even the super-majors aren’t immune from the devastation. Due to the impact the oil price collapse will have on their oil production segments, ExxonMobil, Shell, and Chevron have all gutted their 2020 spending plans to preserve capital largely aimed at maintaining their dividends. Even Phillips 66 (NYSE: PSX), which doesn’t produce oil, is cutting back on capital investments as its refining and marketing segments are likely to be walloped by cratering demand.

What’s an investor to do?

First, I do expect there will be money made by some investors as a result of the oil crash. There will prove to be bargains once we have the benefit of hindsight to know. But with that said, I think most investors should do absolutely nothing in the oil patch today. The demand destruction we are right in the middle of is completely unprecedented, and at the same time Russia, Saudi Arabia, and the United Arab Emirates are pumping more oil than they have in years. Even U.S. production is only just starting to slow, and is still far above demand as the past couple of weeks of inventory builds show.

The cheapest oil stocks are the independent producers, but as I outlined above, that subsector is a minefield. I expect a lot more bankruptcies, and even the best-run independent producers, like Pioneer Natural Resources (NYSE: PXD) with better stronger balance sheets and some liquidity they can access, are about to face the toughest environment in their history. It’s just too early in the story to know how serious the risks will prove to be.

I expect the supermajors like Shell, Chevron, and ExxonMobil will make it through, if not unscathed, then in good enough shape. Similarly, Phillips 66, without a production segment around its neck and plenty of liquidity between cash and cheap debt it can tap, should come out the other side in fine condition. But even this fine collection of companies, with all their cash and low-cost debt, could see a painful 2020 and even early 2021, depending on how quickly global demand picks back up, and how deep the flood of crude still pouring into the markets turns out to be, and how long it takes to soak it up before producers can start ramping up again.