A number of lenders are cutting rates but experts say it may be too early to call it a turning point.

Image source, BBC

Image source, BBC Among those walking through the doors of one Warrington estate agency, it is the buyers – rather than the sellers – who have more of a spring in their step.

“It’s definitely a buyers’ market at the moment,” says Sadia Mian, director of Northwood estate agents.

They are feeling confident enough to “under offer” when making a bid for a property, she says.

This confidence is bred from necessity. People are having to take into account the relatively expensive mortgage repayments they face after buying a home.

Halifax, the UK’s biggest mortgage lender, suggests that first-time buyers are still active in the housing market. There is evidence they are now searching for smaller homes in cheaper areas to offset the high cost of a home loan.

‘Turnaround’

Mortgage rates, which recently touched a 15-year high, have cast a long shadow over the finances of potential buyers.

It is the same for existing homeowners, about 1.5 million of whom will see their current mortgage deal expire by the end of next year.

Many will have been delighted to see major lenders, including the Halifax, Nationwide, NatWest and HSBC, cutting their interest rates on new deals in recent days. Santander is following suit with a reduction on Monday.

“The cuts to fixed rates are now gathering some momentum,” says David Hollingworth, from broker London and Country Mortgages. “That’s good news and signals a turnaround for fixed rates after the rapid increases of recent months.”

But even if this is a turning point, it is far too early to get carried away.

The average rate on a two-year fixed mortgage deal is 6.8%, according to the financial information service Moneyfacts. Despite falling from its peak, that is still only back to the level it was three weeks ago.

Moneyfacts says the typical rate for a longer five-year deal is 6.28%, around the same as a month ago.

“There is no doubt mortgage rates need to reduce a few more times before most borrowers will be happy and confidence returns to the mortgage and property sectors,” says Aaron Strutt, of broker Trinity Financial.

So, why are these cuts happening now?

It is partly a response to more competition for less custom.

Lenders want to manage their workload so they are getting a good, but not overwhelming, number of applications. For some, that has meant reducing rates to tempt borrowers who may have delayed decisions to buy.

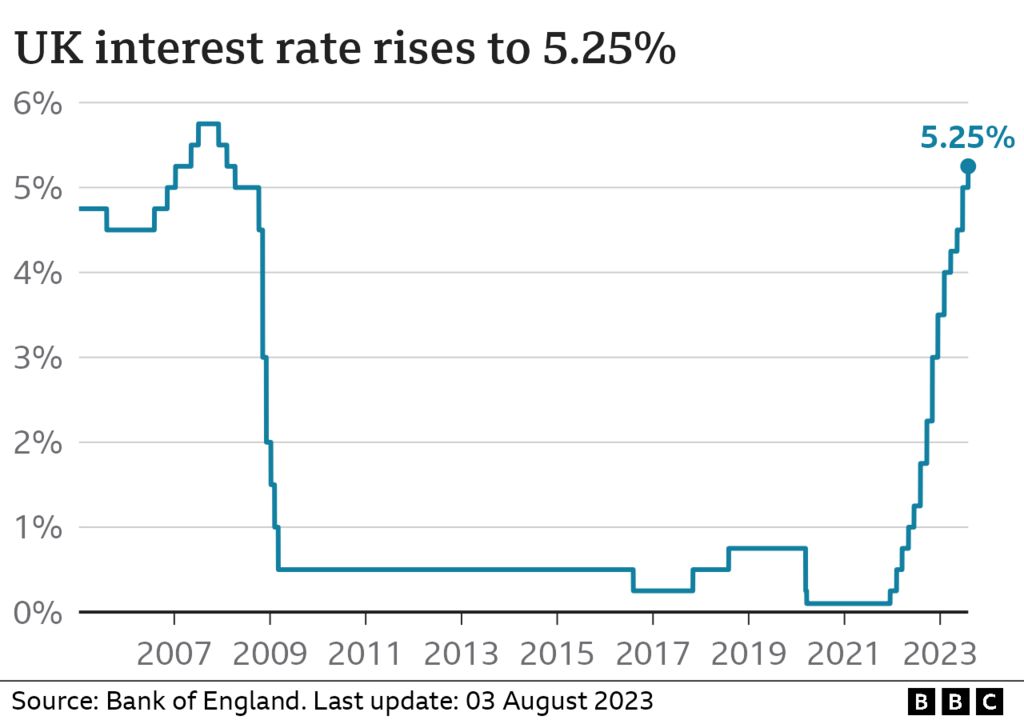

Analysts also say that lenders are responding to expectations that the Bank of England’s interest rate may not stay very high, for as long. The Bank rate is used as a tool to control the rate of rising prices – known as inflation – and recently went up to 5.25%.

However, better-than-expected inflation data published a few weeks ago and, in turn, relatively stable swap rates – which underpin mortgage pricing – have given some confidence to lenders.

The next set of inflation data will be published on Wednesday. Any signs of it staying unexpectedly and stubbornly high could see that confidence quickly evaporate.

“With potential for further base rate rises, and the continuing fluctuation of other factors that influence the rates offered to buyers, it is difficult to predict if we have reached a turning point,” says James Hyde, from Moneyfacts.

It is not only mortgaged homeowners and first-time buyers who will be watching developments closely. So too will two million landlords in the UK who have buy-to-let mortgages, and millions of tenants who will see their rent rise if landlords’ costs remain high for a long time.

Renters are mostly at the mercy of landlords, although they do have certain rights to draw on.

Homeowners have a little more control, and many will be wondering whether to delay signing up for a mortgage if there is a prospect of further falls.

Brokers suggest that a safety-conscious approach may be the best policy.

Image source, Getty Images

“It makes sense to continue to take action to secure a rate now and then keep it under review, to see if a switch to a better rate becomes possible in time,” says Mr Hollingworth. “That at least ensures a deal is in place in case anything derails the current improvement but also leaves enough flexibility to take advantage of any further cuts.”

Most lenders allow homeowners to choose a new product around six months before their current fixed deal expires, often with the option of swapping to a cheaper product if it reduces its rates during that time.

Mr Strutt says the danger of delaying is the chance of defaulting to a lender’s standard variable rate (SVR) when the current deal expires, and many SVRs have interest rates of 9-10%.

Ultimately, everyone agrees that there is little sign of a return to the ultra-low rates of less than 2% that benefitted homeowners for more than a decade before late 2021.

In practical terms, many borrowers face monthly repayments under a new deal that could be hundreds of pounds more expensive than their previous mortgage, and they will need to budget accordingly to try to cope with that financial hit.

What happens if I miss a mortgage payment?

- If you miss two or more months’ repayments you are officially in arrears

- Your lender must then treat you fairly by considering any requests about changing how you pay, such as lower repayments for a short time

- They might also allow you to extend the term of the mortgage or let you pay just the interest for a certain period

- However, any arrangement will be reflected on your credit file, which could affect your ability to borrow money in the future